The Case for Disciplined Conviction in an Apathetic Regime

Periods of market apathy are often misunderstood. When volatility compresses and narratives lose urgency, many participants interpret the environment as a signal to disengage.

The Strategic Value of Volatility

The current market environment — defined by Bitcoin's ~52% retreat from its October 6, 2025 peak of approximately $126,280 to its current stabilization near $65,000–$67,000 — represents a structural "Strategic Pause." From the perspective of Axys Capital, this correction is not merely a price adjustment but a necessary purge of speculative leverage and "zombie" capital.

To understand this regime, one must recognize that we are witnessing the "boy who cried wolf" syndrome in real-time. Investors have heard the promise of institutional adoption for so long that they have become desensitized to its actual arrival — even as approximately $53–54 billion in cumulative net ETF inflows now sit on institutional balance sheets, a figure that peaked near $63 billion in October 2025 before 2026's risk-off rotation trimmed roughly $9–10 billion off that high.

We observe a profound behavioral "anchoring bias". Investors remain anchored to the "punk skateboarder" image of crypto from 2014 and 2017, failing to recognize that the asset class has shaved, put on a suit, and is currently deploying the infrastructure for the next generation of global capital markets.

Structural alpha is rarely forged in periods of euphoria. The current "Extreme Fear" — the Fear & Greed Index stood at 11 as of February 26, 2026, having touched a historic low of 5 on February 6 — creates the precise entry points required for institutional-grade conviction. Unlike the retail-driven "blow-off" peaks of the past, the October 2025 peak was driven by apathy. Apathy tops are intellectually more challenging to navigate than euphoric ones because they lack a single, identifiable capitulation event. Instead, they offer a choppy path that rewards only those who prioritize capital preservation over momentum.

The Macro Clock — Global M2 and the 70-Day Forward Signal

For allocators who demand a when, not merely a why, the Global M2 money supply offers the most historically reliable forward-looking timing mechanism in the asset class.

The structural relationship is well-documented: Bitcoin has historically followed Global M2 expansions with a lag of approximately 60–90 days — with the most cited consensus sitting around 70 days. The mechanism is intuitive: as central banks expand the money supply, excess liquidity searches for yield and risk, eventually flowing into hard-capped assets like Bitcoin. Because Bitcoin absorbs excess capital more efficiently than most instruments — by design of its fixed supply — the price response is disproportionate to the M2 impulse.

The current setup is precisely this: Global M2 has been expanding at over 10% year-on-year while Bitcoin has declined -6% over the same period — a divergence that Fidelity Digital Assets, in their January 2026 report, explicitly identified as a pending reversion catalyst. As Fidelity stated: "As a new cycle of monetary easing begins worldwide and the Fed's QT program concludes, we are likely to see continued growth in money supply throughout 2026. This will serve as a positive catalyst for Bitcoin's price." A 2% uptick in global M2 in late 2024 preceded a ~70% Bitcoin rally with near-textbook precision.

Our Signal: Applied to the present, Global M2's most recent expansion pulse — observed entering Q1 2026 — implies a liquidity-driven price inflection is due within the April–May 2026 window, assuming the historical 70-day lag holds. This does not override our structural thesis; it gives it a temporal anchor. The macro clock is ticking.

Important nuance: The M2-BTC correlation is structural, not mechanical. Since mid-2025, there has been a documented divergence driven by Bitcoin-specific headwinds: ETF outflows, the Yen Carry Trade unwind, and the "L2 Trap." Axys does not treat M2 as a standalone buy signal, but as a necessary-but-not-sufficient condition for the next leg higher — the sufficient condition being a stabilization of institutional net flows.

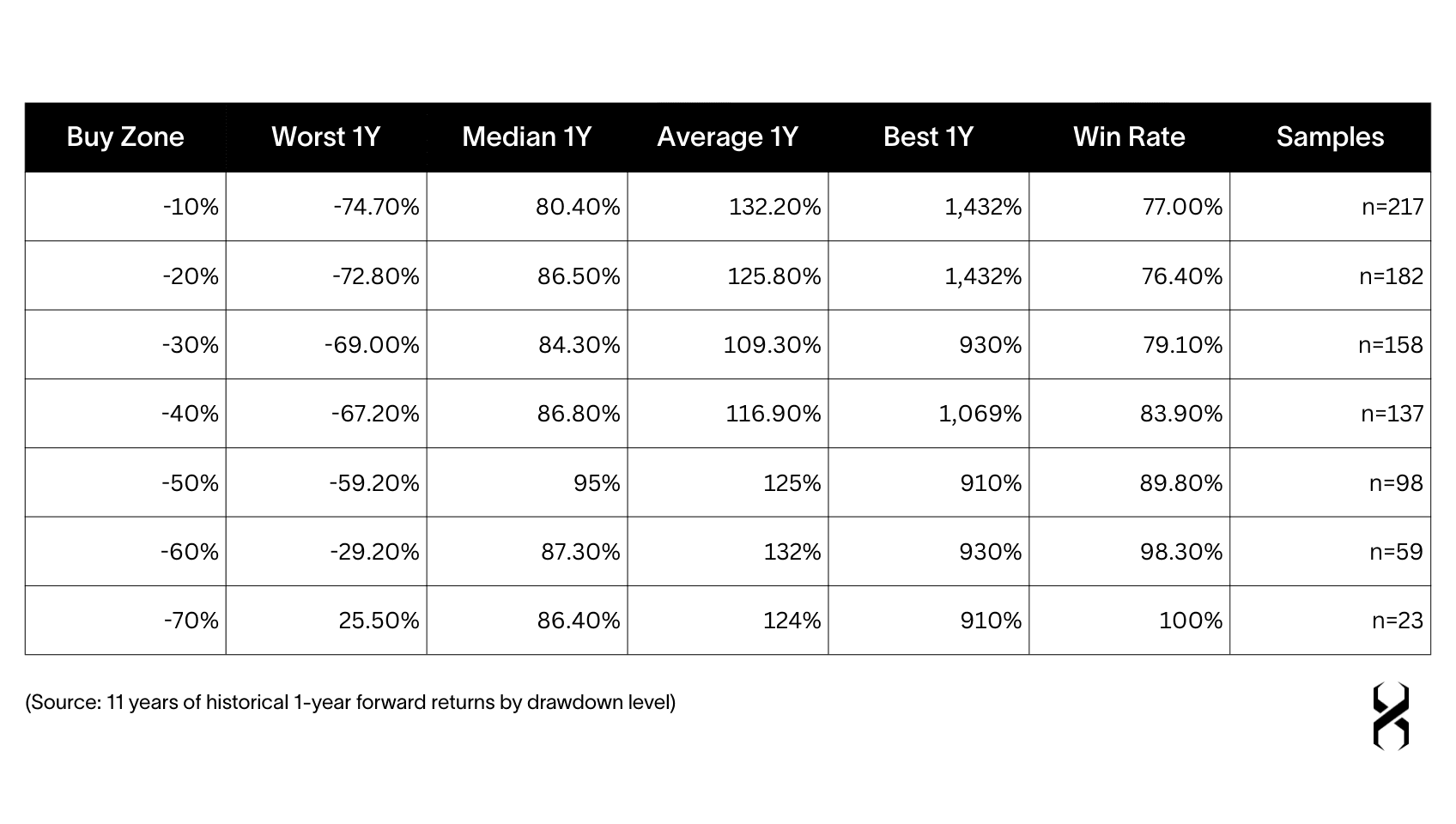

Quantitative Edge — The Anatomy of the Dip

To bolster our thesis of "Disciplined Conviction," we have analyzed 11 years of historical drawdown data. The current regime, sitting at a ~50% drawdown from all-time highs, offers a mathematically superior risk-reward profile compared to almost any other asset class in the global market.

In investment terms, this is the definition of Convexity — where potential profit structurally outweighs potential loss. Three features of this data demand attention:

Compression of tail risk: At a -10% drop, the historical "Worst 1Y" scenario was a -74.7% loss. At our current -50% level, that figure shrinks to -59.2%. The deeper the drawdown, the less "room" there is for further punishment.

Persistence of upside: While downside risk contracts, recovery potential remains explosive. Even at a -60% crash, the historical "Best 1Y" return stands at +930%.

The Win Rate imperative: Buying at -50% offers an 89.8% statistical probability of profitability within 12 months. We would prioritize this certainty of outcome above the noise of the current regime.

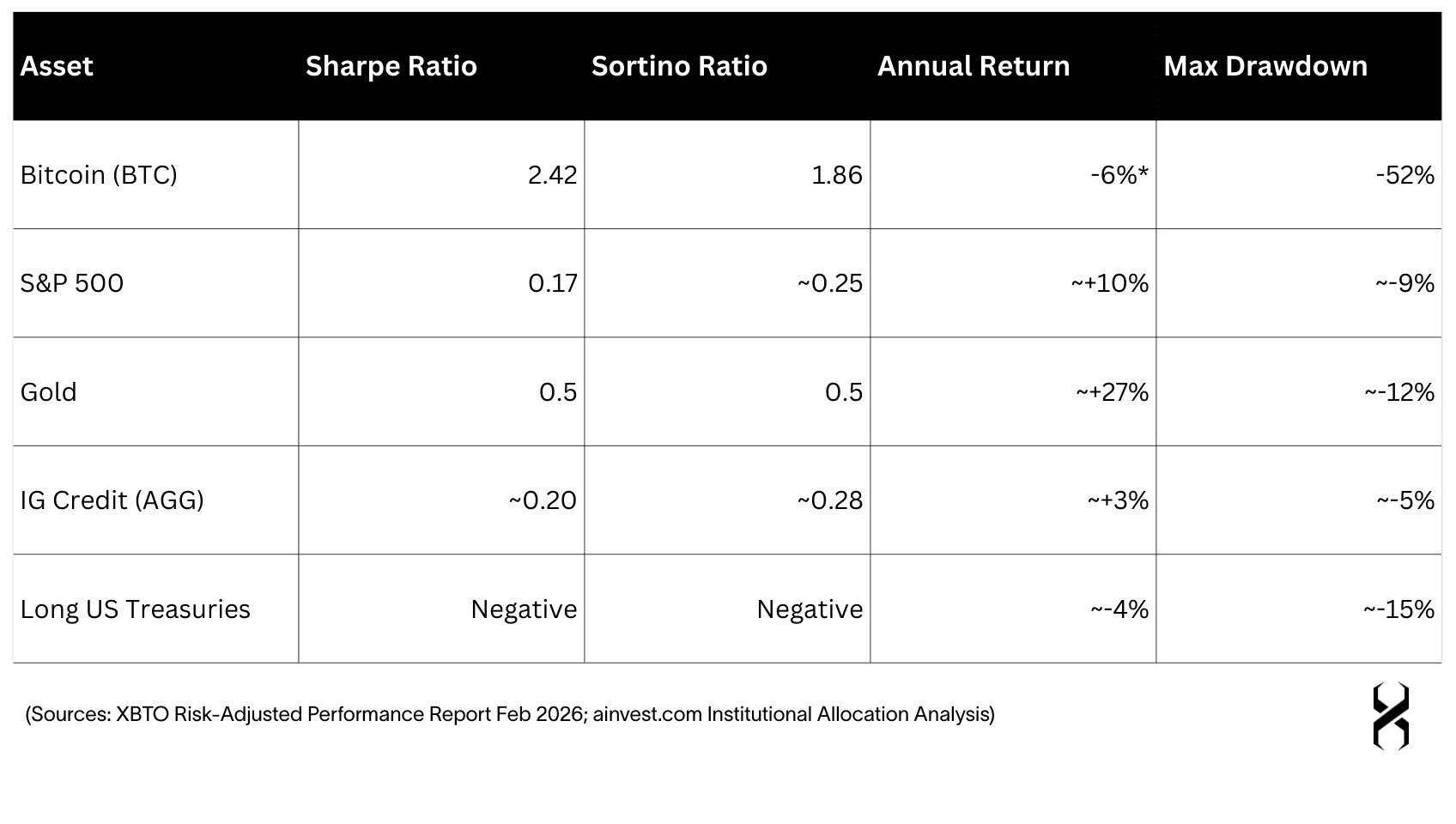

The "Why Not Just Buy Equities?"

The convexity argument only holds if it survives comparison to competing capital allocations. Here it does — definitively.

Risk-Adjusted Return Benchmarking (2025 Full Year)

Bitcoin's Sharpe ratio of 2.42 — placing it among the top 100 global assets by risk-adjusted returns — was achieved before the current -50% dip entry point, which our drawdown data shows compresses downside risk further while preserving upside. The S&P 500's Sharpe of 0.17 in the same period means that for every unit of volatility endured, equities returned a fraction of what Bitcoin delivered. The conventional "safe" allocation was, in risk-adjusted terms, the inferior one.

At the current drawdown level with an 89.8% win rate and a median 1-year forward return of +95%, the forward-looking Sharpe profile for a Bitcoin entry here is arguably the most asymmetric in public markets today. No institutional allocator can rationally dismiss this in favor of 3.5% risk-free yield.

The Law of Diminishing Returns and the Floor Effect

A sophisticated analysis reveals a dual-sided "Diminishing Return" effect that creates a structural floor for our thesis.

Downside Diminishing Returns: As drawdowns deepen, each additional percentage of loss becomes mathematically harder to achieve. To move from -80% to -90%, the remaining market value must be halved again. We are currently in the "Value Vacuum" zone where the marginal pain of further downside begins to diminish — the most speculative capital has already been purged, and February 2026's $1.26 billion single-day liquidation event on February 5 is emblematic of precisely that washout

Upside Maturation: We must acknowledge that the era of 5,500% annual returns, as seen in 2013, is structurally evolving due to the sheer size of the market. As Bitcoin integrates into the $285 trillion global stock and bond market, 100x moves yield to what we term Institutional Stability — lower amplitude, but radically improved risk-adjusted returns.

Critically, while the magnitude of returns normalizes as the asset class matures, the Win Rate does not. The certainty of a positive 1-year forward return trends toward 100% as the drawdown deepens, regardless of whether the median return is +150% or +85

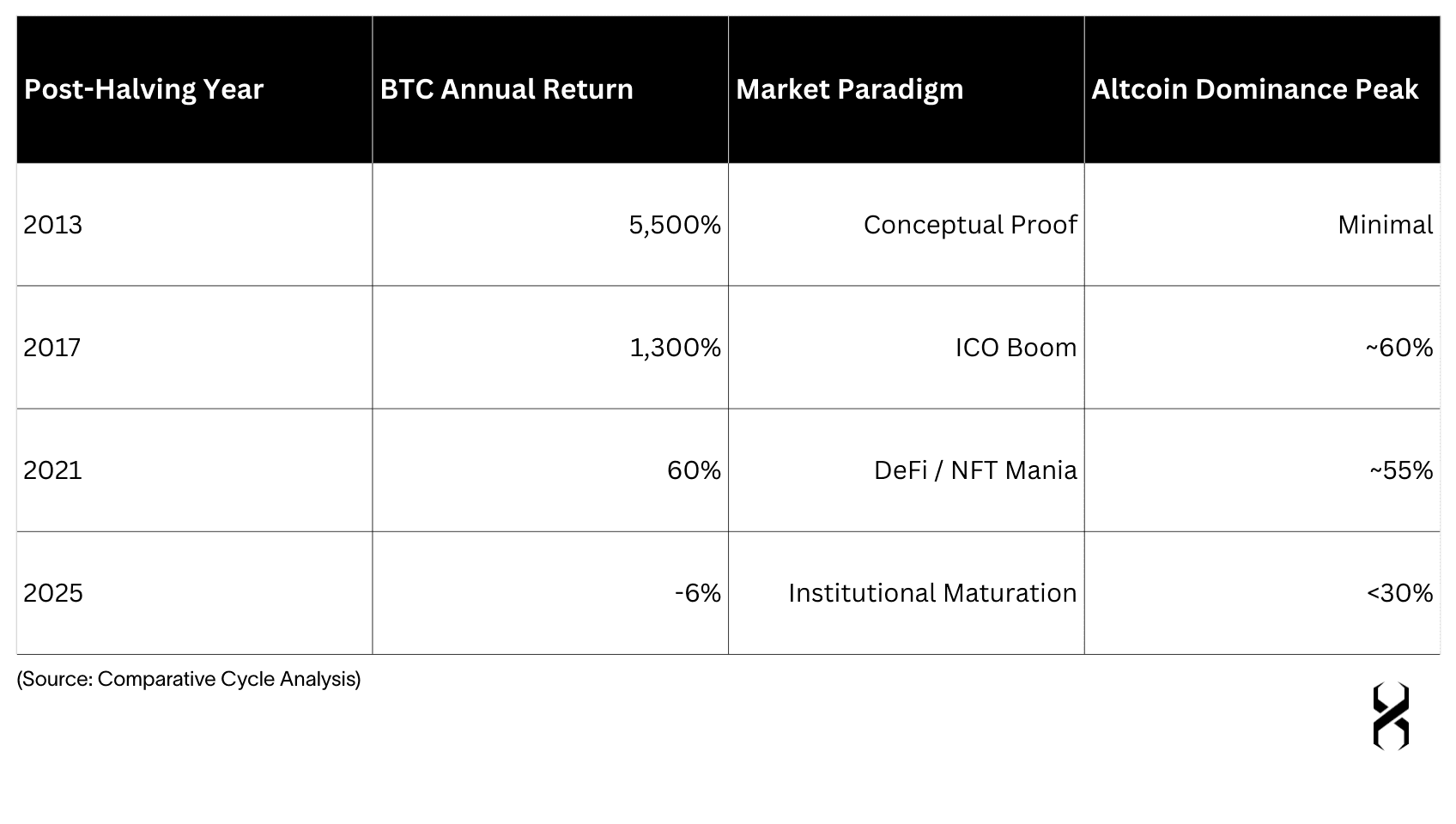

The "Alt Season" Autopsy — Why the Old Playbook Mutated

The 2025 regime shattered the quadrennial script by finishing the post-halving year in the red — a historical first. This mutation was driven by the "Vampire Effect" of spot Bitcoin ETFs: with approximately $54–63 billion in cumulative net inflows at their peak, these vehicles created a structural capital siphon. Unlike prior cycles, ETF capital is mandate-bound — pension funds do not "rotate" into mid-cap utility tokens

The Evolution of Post-Halving Realities

The second-order effect is terminal dilution. We are navigating an ecosystem that has surpassed 50 million unique tokens according to Dune Analytics data, with approximately 5,300 new launches daily and only ~10,000 tokens remaining meaningfully active. This makes a broad-based "rising tide" mathematically impossible. We are no longer investing in a "crypto market"; we are investing in a bifurcated landscape where liquidity clusters exclusively around assets with institutional-grade utility.

The L2 Trap and Liquidity Fragmentation

In a regime where the "risk-free rate" sits at 3.5%–3.75%, liquidity has replaced "innovation" as the primary determinant of survival. The market has been further pressured by the Yen Carry Trade unwind — a macro event where rising Japanese yields forced the liquidation of risk assets, amplifying the already stressed crypto drawdown.

This coincided with the "L2 Trap." The proliferation of Layer-2 solutions has fragmented global state into asynchronous "Liquidity Silos," deterring retail participation through bridging complexity and elevating gas-cost uncertainty. Consequently, we have witnessed a significant compression in market structure:

Volatility Drop=Vpre(4.2%)−Vpost(1.8%)Vpre(4.2%)≈57%

This 57% drop in daily volatility reflects the "TradFi-ization" of price discovery — institutional participants operate on weekly or monthly rebalancing cycles, not the intraday reflexivity that historically defined crypto. Axys Capital is intentionally avoiding "fragmented" assets in favor of established liquidity hubs with unified state and verifiable on-chain activity.

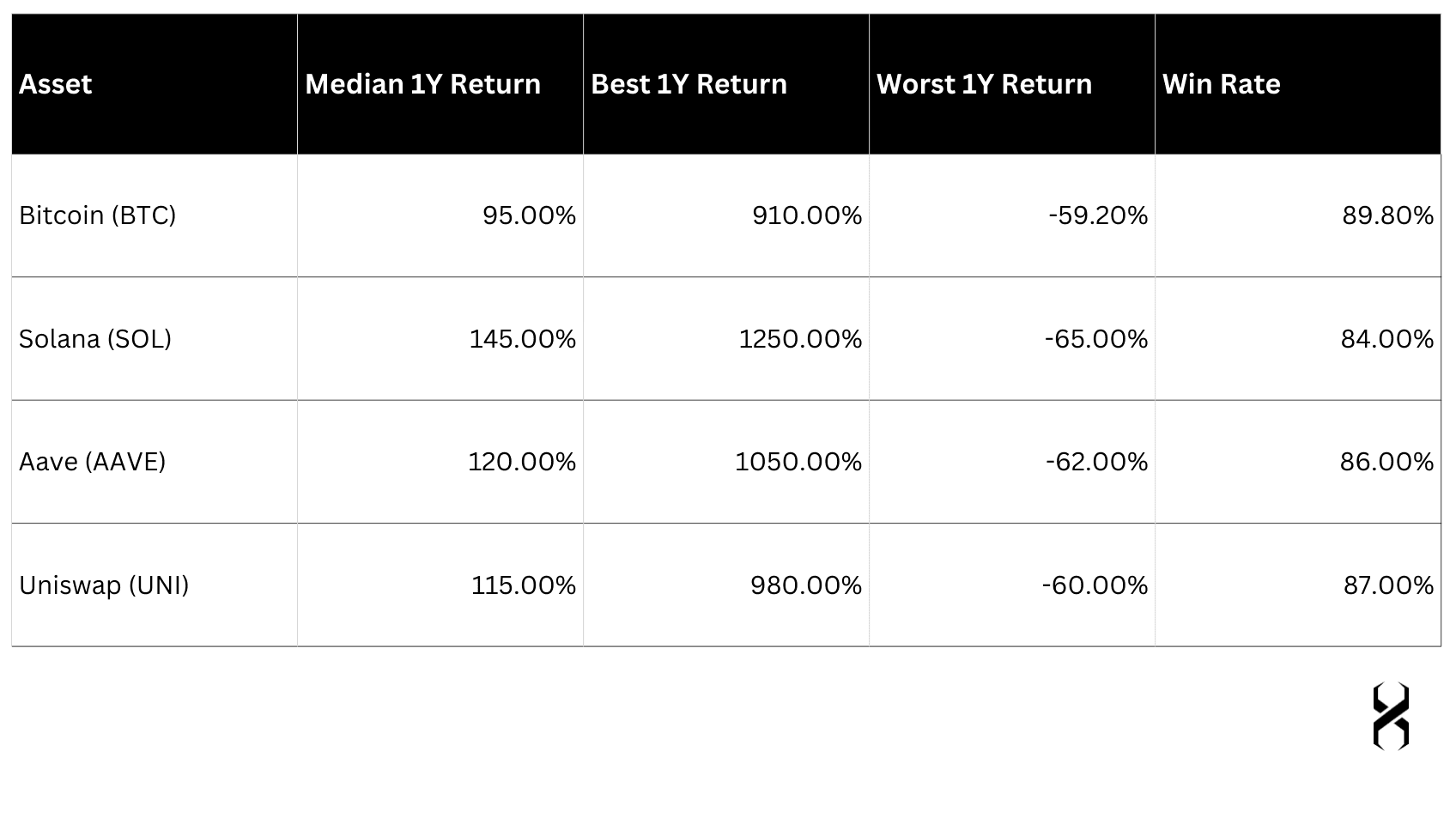

Conviction Spotlight

We maintain high-conviction positions in assets with verifiable network utility: BTC, SOL, AAVE, and UNI.

Bitcoin (BTC): Our "Macro-Linked Scarce Asset." BTC now correlates more closely with gold than speculative tech, acting as a defensive anchor within the portfolio. The February 25, 2026 single-day inflow of $506.5 million into spot Bitcoin ETFs — led by BlackRock's IBIT with $297.4 million — signals institutional sentiment is returning to "cautious accumulation" after the de-risking period.

Solana (SOL): Occupies the "Institutional Adoption Curve" by virtue of its unified state architecture. With 32 million of the world's ~50 million crypto tokens launched on its network, Solana captures the high-frequency, low-latency applications that fragmented L2 ecosystems cannot service.

The BlackRock/Uniswap Paradigm: On February 11, 2026, BlackRock — in partnership with Securitize — integrated its $2.1–2.4 billion BUIDL tokenized money market fund directly with UniswapX infrastructure, enabling 24/7 on-chain trading for whitelisted participants. As Robert Mitchnick, Global Head of Digital Assets at BlackRock, stated: "The integration of BUIDL into UniswapX marks a major leap forward in the interoperability of tokenized USD yield funds with stablecoins." This validates our weighting in UNI and AAVE as the back-end infrastructure for the next architecture of global finance. BlackRock also acquired an undisclosed amount of UNI governance tokens as part of the arrangement, underscoring the structural nature of this commitment.

Core Asset Sensitivity Analysis (1-Year Forward Projection from -50% Drawdown)

A thesis built on "strong hands accumulating" must be evidenced, not asserted. The on-chain data as of late February 2026 provides precisely that confirmation across three independent metrics.

Long-Term Holder Supply — 13.96M BTC. CryptoQuant data shows the long-term holder (LTH) balance has rebounded to approximately 13.96 million BTC — coins unmoved for 155+ days — after briefly dipping during the October 2025 peak distribution phase. This represents roughly 70% of circulating supply locked in conviction hands. Historically, LTH supply recovering at drawdown levels of -50%+ has preceded every major bull cycle resumption.

MVRV 365-Day at -29% — A Historic Buy Signal. Bitcoin's 365-day MVRV ratio currently sits at -29%, placing it in what Santiment classifies as a "historic low-risk zone." This means the average long-term market participant is sitting at an unrealized loss of approximately 29% relative to their cost basis — the precise psychological condition that historically precedes capitulation exhaustion and structural reversal. The last time MVRV reached comparable levels was the 2022 bottom and the 2019 accumulation floor — both of which were followed by >200% recoveries within 12 months.

Leverage Ratio Collapse — Structural, Not Panic. Bitcoin's leverage ratio has plummeted 28% as of February 27, 2026, falling below historic lows. This is critical: it signals that the market is de-leveraging structurally rather than through panic liquidation. Forced selling exhausts itself; structural de-leveraging creates a cleaner, healthier base. When leverage re-enters this market, it does so against a more compressed cost basis — amplifying the recovery move.

Exchange Reserve Watch: Between February 18–24, exchange BTC reserves rose by 23,589 BTC — a modest 0.86% increase — while price fell 5.89%. This divergence, where supply moving to exchanges fails to produce commensurate price impact, is a classic sign of absorption: patient capital is buying what anxious capital is selling

The Roadmap to Recovery

The 2025 cycle "topped on apathy" rather than euphoria. This distinction is crucial: it means speculative "tourists" have been washed out — over $2 trillion in total crypto market cap was erased in a single 48-hour window in early February 2026 — leaving only the "strong hands."

Recency Bias and the Wall of Worry

Just as investors spent 2024–2025 "fighting the Fed," they are now likely to fight the next uptrend, conditioned by the "liquidity starvation" of the past year. This creates a Wall of Worry: when the market eventually turns — driven by a return of favorable Net Liquidity — the initial rally will be met with disbelief. That skepticism is the powder keg for the massive FOMO that follows when the trend becomes undeniable.

The 2019 Parallel: Clearing the Deck

The current environment draws a striking parallel to the 2019 cycle. That era of "echo bubbles" and altcoin bleeding was necessary to reset valuations and wipe out "zombie" projects. It was precisely that period of despair that seeded the accumulation phase enabling "DeFi Summer." The current "disappointment" is performing that same surgical function: clearing the deck so capital can concentrate on the next dominant narrative — the $285 trillion tokenization era.

The Three Certainties We Carry Into Q2 2026

Amid all the noise, we anchor to three things we consider near-certain:

1. The macro regime will shift. It always does. The Federal Reserve's QT cycle is nearing its terminal phase. Global M2 is expanding. The political will — now formalised through the joint SEC-CFTC "Project Crypto" initiative — to build institutional infrastructure around digital assets is the most durable regulatory tailwind this asset class has ever received. When loose money returns, and it will, the contrast against the current psychological baseline will be violent and swift. The Wall of Worry that has been built brick by brick throughout 2025 and early 2026 will become the launchpad for the next leg.

2. The infrastructure is already built. BlackRock's BUIDL fund is live on UniswapX. The DTCC tokenization sandbox is active. Sovereign wealth funds from Abu Dhabi to Norway are at the threshold of formal digital asset mandates. The $285 trillion tokenization era is not a prediction. It is a construction site. And the assets Axys Capital holds — BTC as the macro anchor, SOL as the unified-state execution layer, UNI and AAVE as the DeFi rails of institutional finance — are not bets on that future. They are the infrastructure of it.

3. The asymmetry is mathematically undeniable. At a -50% drawdown entry, with an 89.8% win rate, a median 1-year forward return of +95%, there is no competing asset class in public markets today that offers this profile. Not equities at a 0.17 Sharpe. Not gold at 0.50. Not investment-grade credit at 3.5%. The numbers are not a narrative. They are a mandate.

Disclaimer

This report has been prepared by the research department of Axys Capital and is for informational purposes only. The analysis and opinions presented are based on publicly available data, price action study, and smart money concepts, and reflect our independent judgment as of the date of publication. This material does not constitute, nor should it be construed as, investment advice, a recommendation, or an offer or solicitation to buy or sell any financial instrument or to participate in any trading strategy.

Axys Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or reliability of any information contained herein. Market conditions, data, and analysis may change without notice, and Axys Capital does not accept responsibility for any losses or damages arising from the use of this report or its contents. Recipients should conduct their own research and consult with qualified advisors before making any investment decisions.

Past performance is not indicative of future results. All trading and investment strategies involve risk, including possible loss of principal.