The Great Divergence: Immunity, Liquidity & the new regime in sound money

The Great Divergence: Immunity, Liquidity & the new regime in sound money

Dear Partners,

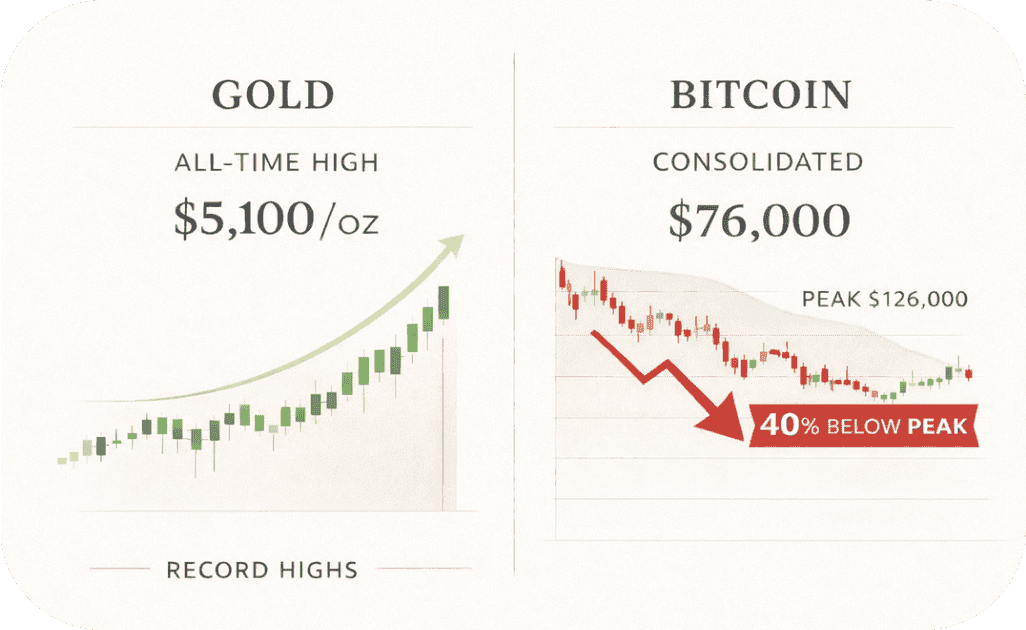

If 2025 was the year of "Digital Gold" theoretical, January 2026 has been the month of empirical reality. We are currently witnessing a historic decoupling in the non-sovereign asset space. Gold has severed its traditional correlation with real rates to breach 5,100/oz, delivering its strongest annual performance since 1979. Conversely, Bitcoin has struggled to find a floor near $88,000-$84,000, and eventually drop to $76,000, punished by a liquidity vacuum that has seen over $1.1 billion exit spot ETFs in a matter of weeks.

Investors are asking a valid question: If the world is fracturing, why isn't the hardest money on earth rallying?

The answer lies in the specific nature of the current fear. The geopolitical shocks of late Q4 2025—specifically the Greenland tariff disputes and the weaponization of the dollar against Venezuela—have driven capital not just toward scarcity, but toward immunity. Central banks, led by Poland and Brazil, are aggressively accumulating gold because it carries no digital counterparty risk and cannot be "turned off" by a sanctions regime.

Bitcoin, while scarce, is currently trading not as a geopolitical shield, but as a levered proxy on global liquidity—liquidity that is currently retracting.

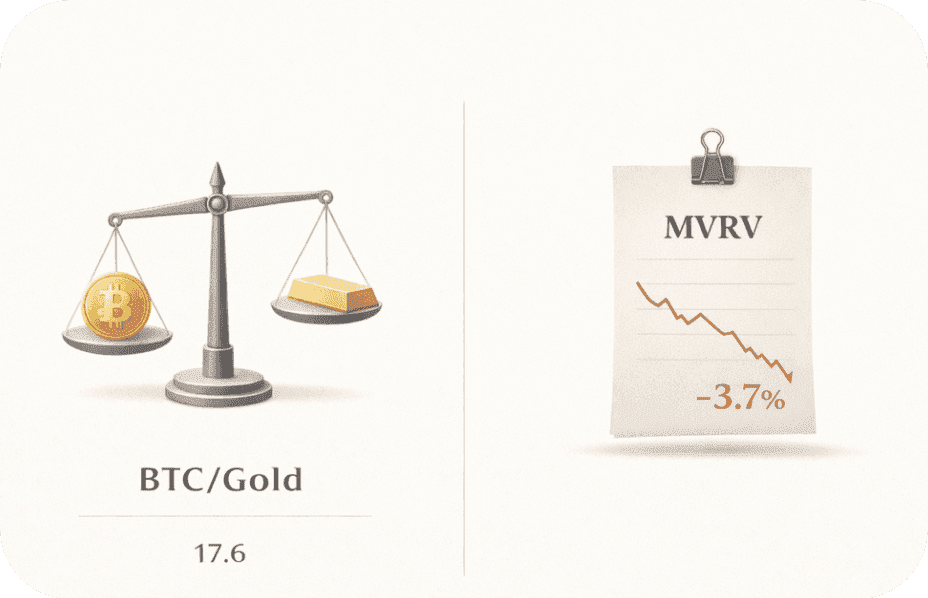

However, market dislocations of this magnitude create the most asymmetric opportunities. The Bitcoin-to-Gold ratio has collapsed to 17.6, a level historically associated with deep value zones rather than cycle tops. While the market currently pays a premium for the "Shield" (Gold), it is aggressively discounting the "Spear" (Bitcoin).

In the following memorandum, we detail why this divergence is a feature of institutionalization rather than a failure of the asset class, and why the current regulatory calcification via the GENIUS Act suggests that the "Spear" is merely coiling, not breaking.

The Reality of Relative Performance

In the investment craft, the most dangerous path is confusing a temporary dislocation with a terminal failure of thesis. We find ourselves today at a classic inflection point where the market pendulum has swung toward extreme pessimism for digital assets, while bullion enjoys a period of near-universal acclaim. The price action is, as Howard Marks would observe, the messenger of current sentiment: Gold has ascended to all-time highs near 5,100/oz, while Bitcoin consolidated at $88,000—a 30% drawdown from its October 2025 peak of $126,000, and eventually got a large correction to $76,000

To the first-level thinker, this divergence suggests that the "digital gold" narrative has collapsed. Second-level thinking, however, requires us to ask why the market is currently prioritizing physical safety over digital scarcity. Our "sound money" thesis remains fundamentally sound, but we are navigating a period of path dependency where geopolitical friction has temporarily favored the tangible over the programmable. We are currently in the "trough of disillusionment," a phase that historically tests the conviction of the disciplined while providing the seed for the next cycle of outperformance.

The "Shield" vs "Spear" framework

The decoupling of traditional asset correlations in early 2026 necessitates a more nuanced framework. We can no longer view alternative assets as a monolithic bloc. Instead, we must distinguish between the "Shield" and the "Spear."

Gold as the "Shield": Bullion is currently the ultimate sovereign insurance. As the "Greenland Tariff" threats heighten global trade volatility and the memory of the seizure of Venezuelan assets lingers, nations like Poland and Brazil are aggressively rotating out of US Treasuries. For China, gold has become a vital "liquidity sponge," allowing the state to absorb high domestic savings and manage capital flight stemming from a weak property sector and aging demographics. It is an asset with no counterparty risk, providing a bunker for capital in a de-globalizing world.

Bitcoin as the "Spear": Bitcoin remains our high-beta exposure to global liquidity and technological adoption. However, that spear has been blunted by an acute evaporation of risk appetite. The Japan bond market meltdown on January 20 triggered a global risk-off rotation that caught the digital asset complex in its wake. This fragility is exacerbated by a 78% probability of a US government shutdown—specifically driven by fractured negotiations over DHS funding and ICE enforcement.

In this regime, the market is choosing the Shield to weather the storm, leaving the Spear to wait for the return of liquidity. But does the Shield’s rise mean the Spear is broken?

Institutional Mechanics and the Digital Asset Treasury (DAT) Failure

The current price stagnation in Bitcoin is less a rejection of its scarcity and more a reflection of "institutional plumbing" under stress. Between January 20 and January 26, we witnessed $1.1 billion in weekly outflows from spot Bitcoin ETFs, led by heavy redemptions in BlackRock’s IBIT and Grayscale’s GBTC. This stop-start pattern suggests tactical de-risking rather than a long-term exodus.

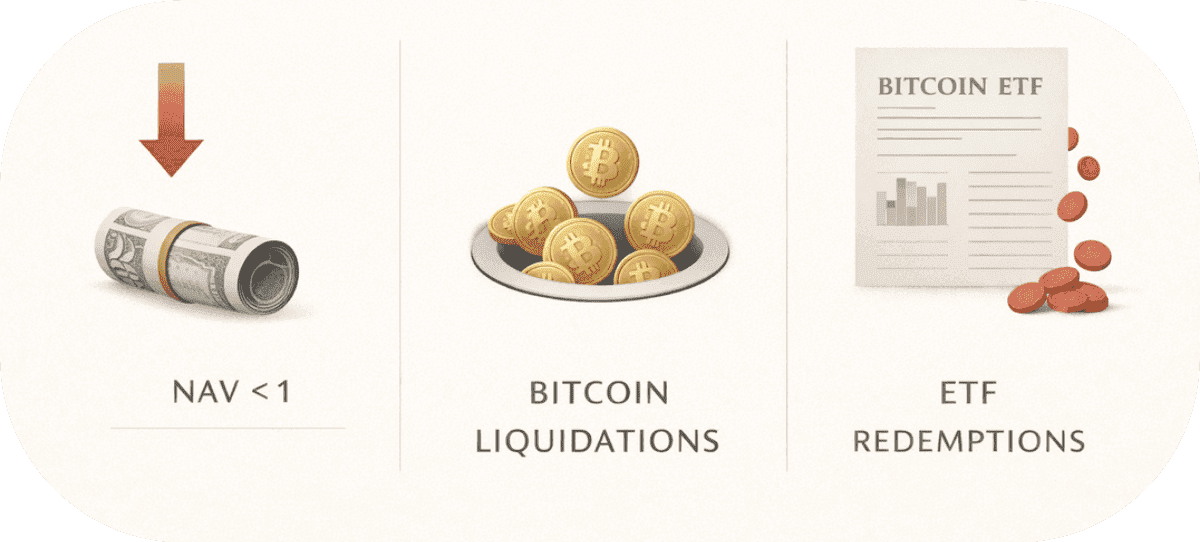

Crucially, the Digital Asset Treasury (DAT) model is facing a structural test. The NAV premium compression for firms like MicroStrategy has inhibited their ability to act as a market backstop. A DAT’s efficacy relies on a market-to-NAV (mNAV) ratio holding above 1; when it falls, the "printing press" for further accumulation stops.

Furthermore, the mechanical nature of this sell-off was evidenced by the $19 billion in liquidations on a single day—the largest in crypto history—which cleared the speculative floor. With the cost to mine 1 BTC now exceeding the BTC price, miners have become forced sellers to cover operational debt. Paradoxically, the SEC’s recent removal of position limits on Bitcoin and Ethereum ETF options (for Nasdaq ISE and PHLX) provides the infrastructure for a more mature, hedged recovery, even as the "plumbing" currently feels backed up.

Geopolitics: The "Fire Alarm" vs. Consensus Resilience

The Goldman Sachs 2026 Outlook remains steadfast in its narrative of "US Resilience," explicitly advising clients not to use gold or bitcoin as a hedge. We find this consensus view to be a lagging indicator. Gold’s 70% gain over the last 12 months is not a speculative anomaly; it is a systemic fire alarm.

While Wall Street focuses on "US Exceptionalism ", the reality of a 38 trillion US debt and 1 trillion in annual interest payments has turned gold into a hedge against fiscal sustainability itself. The freezing of sovereign assets has signaled to the world that "US Exceptionalism" is no longer a neutral guarantee. Gold acts as the market’s way of pricing in the eventual necessity of a more accommodative, inflationary monetary policy to manage the debt burden. The fire alarm is ringing; Goldman Sachs is simply choosing to ignore the noise.

The Silver Lining: Identifying the "Fat Pitch"

As the pendulum of sentiment reaches its bearish extreme, we must look for the "fat pitch." In our view, the indicators for a significant H2 2026 recovery are coalescing:

Valuation Extremes: The BTC/Gold ratio currently sits at 17.6, hitting the lower end of its historical range. Furthermore, Bitcoin’s 30-day MVRV (Market Value to Realized Value) is at -3.7%, signaling that the asset is mildly undervalued and that average holders are underwater—a zone that has historically preceded price reversals.

Regulatory Rails: While the Clarity Act markup was delayed following Coinbase’s withdrawal of support over stablecoin yield bans, this is a temporary political setback. The long-term trajectory of the GENIUS Act provides the necessary rails for the entry of pension and sovereign wealth funds.

Supply Shock Dynamics: On-chain exchange reserves have reached their lowest levels since 2018. The supply of liquid coins is thinning. Once the macro volatility from the government shutdown and tariff rhetoric stabilizes, this constrained supply will meet a resurgence in demand, likely triggered by the end of the Federal Reserve’s tightening cycle.

Conclusion: Conviction Amidst Divergence

We were correct on the asset class (sound money), but the current regime rewards the physical. Holding underperforming assets during a "Great Divergence" is painful, but it is exactly when reflexivity works in reverse that the most asymmetric entries are formed. We are not retreating; we are rebalancing for the eventual rotation back into digital scarcity.

Disclaimer

This report has been prepared by the research department of Axys Capital and is for informational purposes only. The analysis and opinions presented are based on publicly available data, price action study, and smart money concepts, and reflect our independent judgment as of the date of publication. This material does not constitute, nor should it be construed as, investment advice, a recommendation, or an offer or solicitation to buy or sell any financial instrument or to participate in any trading strategy.

Axys Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or reliability of any information contained herein. Market conditions, data, and analysis may change without notice, and Axys Capital does not accept responsibility for any losses or damages arising from the use of this report or its contents. Recipients should conduct their own research and consult with qualified advisors before making any investment decisions.

Past performance is not indicative of future results. All trading and investment strategies involve risk, including possible loss of principal.