The global financial landscape has reached a structural inflection point.

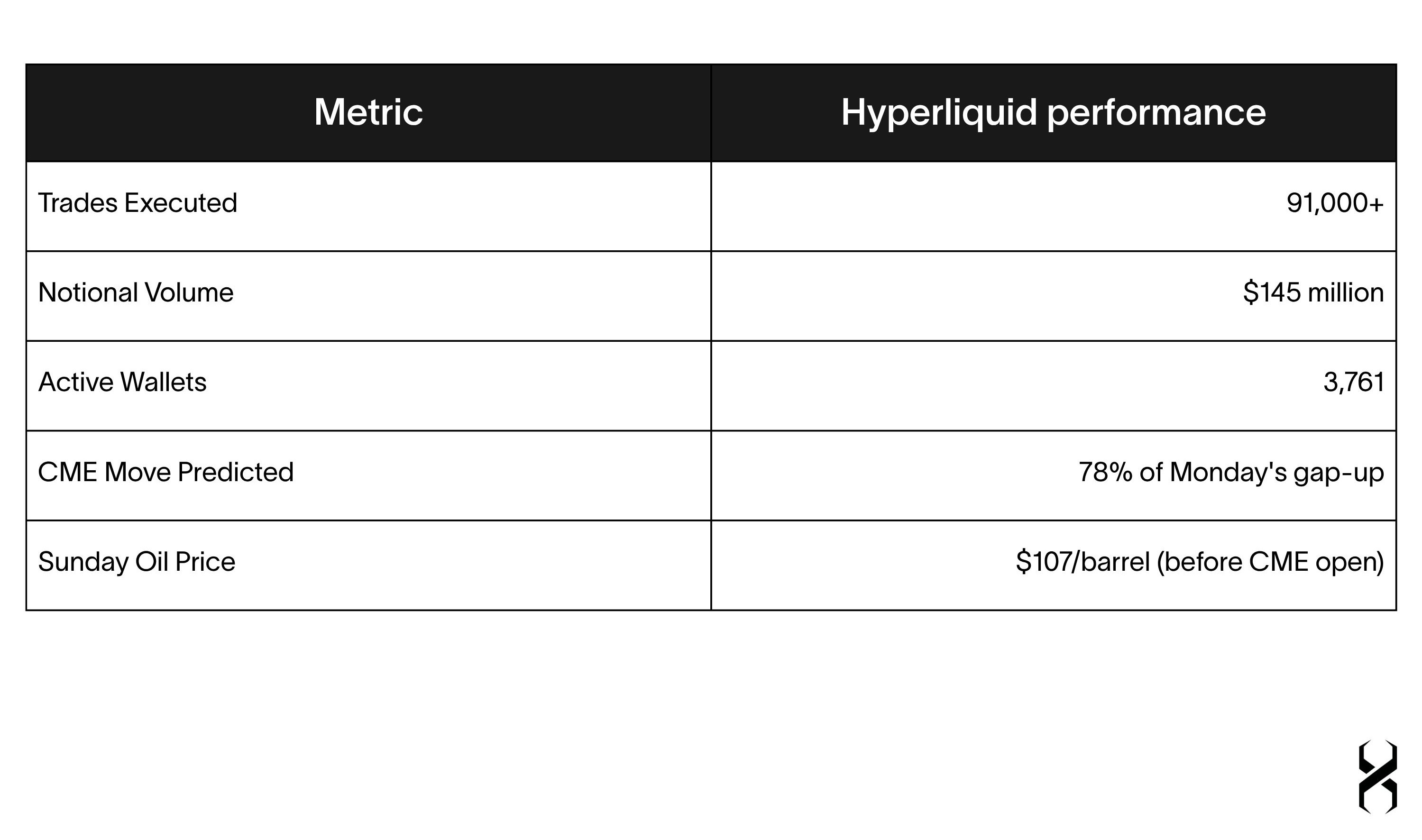

In the 49 hours while traditional markets were dark, Hyperliquid processed 91,000 crude oil trades and priced 78% of the CME's Monday opening move — before legacy markets quoted a single tick.

Executive Summary

The global financial landscape has reached a structural inflection point where the legacy distinction between crypto-assets and traditional assets is no longer functional. At Axys, our thesis for March 2026 centers on the emergence of the Exchange of Everything — a singular, 24/7 liquidity hub where commodities, equities, indices, and digital assets coexist within a unified collateral pool.

Hyperliquid has transcended its origins as a high-performance decentralized exchange to become the primary infrastructure layer for this transition. By leveraging a purpose-built Layer-1 blockchain and a unified USDC collateral pool, the protocol has achieved structural escape velocity from the DEX vertical — generating $843 million in FY2025 revenue with a team of 11 people, surpassing Ethereum in protocol revenue, and becoming the only decentralized exchange ever to enter the global Top 10 perpetual futures exchanges.

The geopolitical volatility of February and March 2026 — specifically the escalation of the conflict in Iran — served as the definitive proof-of-concept. While traditional markets were physically constrained by weekend closures and opening bells, Hyperliquid provided continuous, institutional-grade price discovery for crude oil and global indices. In the 49 hours between the Iran strikes and the CME's Monday open, Hyperliquid processed 91,000 trades across 3,761 wallets and priced in 78% of the eventual Monday opening move before legacy markets quoted a single tick.

The Proof of Concept: Oil, War, and 24/7 Markets

The transition of decentralized derivatives from a retail-oriented novelty to a pillar of primary market infrastructure was validated during the stress test of late February 2026. We characterize the events following Operation Epic Fury as the definitive moment where legacy financial systems failed to maintain global price discovery while on-chain infrastructure succeeded.

Chronology of Crisis

On Friday, February 27, 2026, at 3:38 p.m. EST, authorization for coordinated strikes on Iran was signed on Air Force One. By February 28, 9:45 a.m. IRST, Operation Epic Fury commenced with U.S. and Israeli airstrikes targeting critical Iranian military sites, nuclear facilities, and leadership centers. Over 200 fighter jets and more than 1,200 bombs were deployed in the first 24 hours.

This shock occurred while the world's primary energy exchanges — the CME and ICE — were closed for the weekend. The dark period lasted 49 hours. Iran responded with Operation True Promise IV, launching missiles at U.S. bases across the region and effectively closing the Strait of Hormuz — an energy artery responsible for transporting 20-25% of global maritime oil supply. As 150 freight ships stalled, traditional energy investors were paralyzed.

Hyperliquid's CL-USDC perpetual crude oil contract traded without interruption.

Market Response During the 49-Hour CME Shutdown

The Volume Explosion

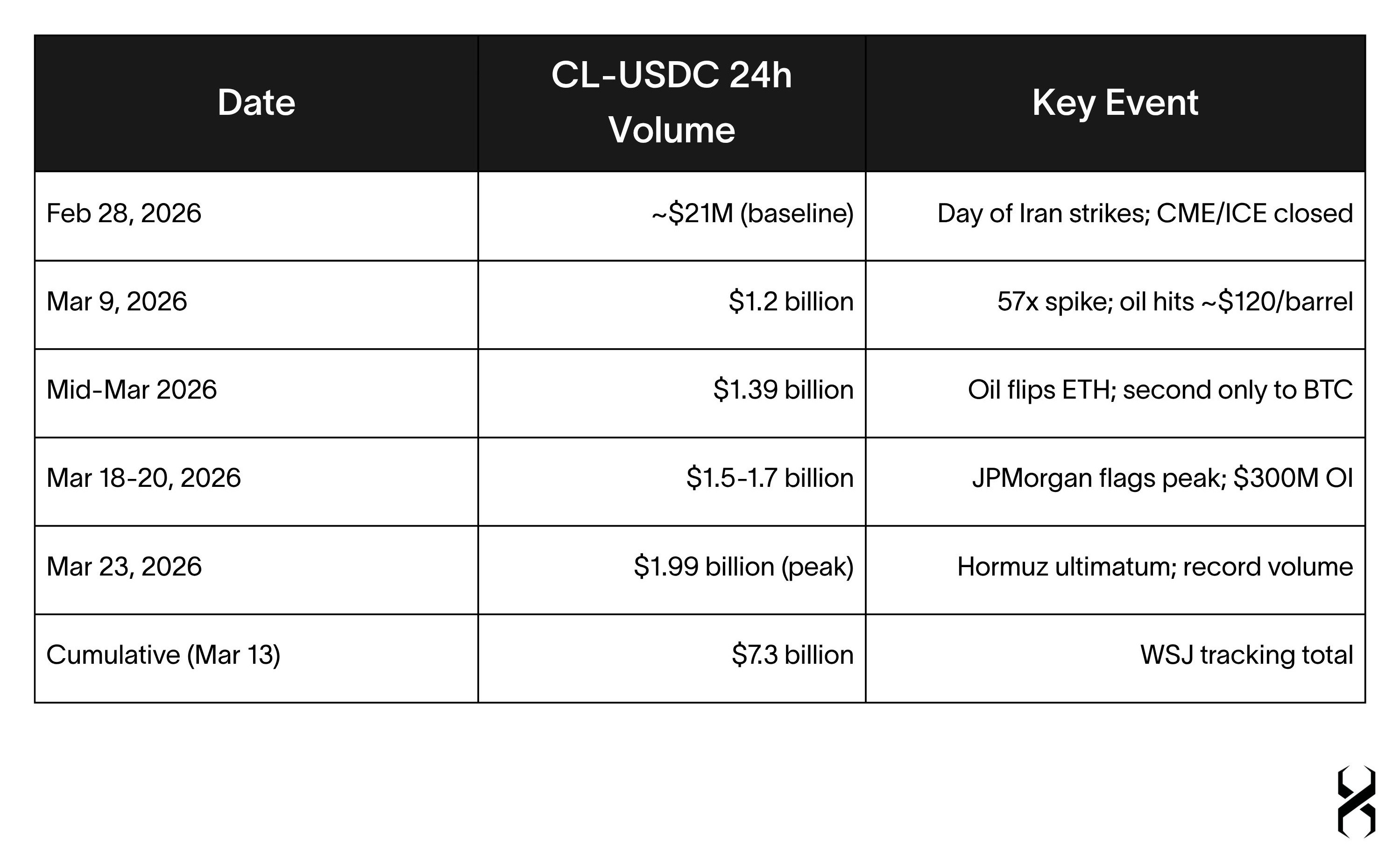

The delta between legacy paralysis and on-chain activity was extraordinary. Hyperliquid's crude oil contract surged from a baseline of approximately $21 million per day to a peak of $1.99 billion in 24-hour volume — a 95x increase. Cumulative oil trading volume reached $7.3 billion by March 13, as tracked by the Wall Street Journal.

By March 9, Bloomberg reported that the WTI perpetual contract had "flipped the Ether token to become the platform's second-most traded market" — a tokenized crude oil contract out-trading the world's second-largest cryptocurrency on a crypto-native exchange. Short positions worth $75 million were liquidated in a single day as oil prices surged over 30%.

The Broader Commodity Complex

The commodity phenomenon extended well beyond oil. By late March 2026, silver perpetuals on Hyperliquid were generating $685 million in daily volume — eclipsing both WTI and Brent, and dwarfing Solana and XRP. Gold perpetuals were running at approximately $700 million in weekly volume, representing the deepest on-chain gold liquidity anywhere in decentralized finance. Combined commodity open interest stood at $730 million.

Institutional Validation

JPMorgan's research team, led by analyst Nikolaos Panigirtzoglou, issued a dedicated note on the phenomenon — noting "significant traction among traders, particularly non-crypto ones, seeking continuous exposure to assets like oil during periods when traditional markets are closed." Goldman Sachs revised its 2026 Brent forecast upward to $85/barrel from $77, with a tail-risk scenario of $135/barrel in the event of a sustained 10-week Hormuz closure. IEA Executive Director Fatih Birol characterized the crisis as "two oil crises and one gas crash put all together" — worse than the 1970s — as the world lost 11 million barrels per day from global supply. The IEA released a record 400 million barrels from strategic reserves, more than double the 2022 release following Russia's invasion of Ukraine.

This was not a crypto event. This was a global macro event where a decentralized protocol served a function that the established financial system could not provide. When CME reopened at a 7.22% gap on Monday, Hyperliquid had already absorbed the volatility, provided real-time exits for hedgers, and established itself as the primary market for global macro shocks during off-hours.

The Macro Thesis: Why Geopolitics Made Crypto Infrastructure Essential

For institutional allocators, the most consequential takeaway from the Iran crisis is not about any single protocol or token. It is about the structural inadequacy of the global market system to function during the kind of geopolitical events that most demand continuous price discovery. The February 2026 weekend exposed a vulnerability that has existed since modern futures exchanges were designed — and it took an on-chain system to fill the gap.

The Infrastructure Gap That Traditional Markets Cannot Close

The world's commodity markets operate on infrastructure built for an era when major geopolitical events could be processed during business hours. CME Group's electronic platform, Globex, closes for maintenance windows and observes weekend shutdowns. ICE follows similar schedules. These closures are legacy artifacts of physical trading floors — preserved through institutional inertia and regulatory convention, not because they serve any protective function for market participants.

The consequences of this design became acute when 200 fighter jets struck Iranian military sites on a Saturday morning. For 49 hours, there was no regulated venue on earth where an energy trader could hedge crude oil exposure, where a portfolio manager could reduce commodity risk, or where a sovereign wealth fund could express a view on the single most important variable in the global economy. The gap was not a technology failure — CME's systems were functioning. It was a structural decision embedded in the market's operating rules that left every participant exposed to asymmetric overnight risk during a genuine crisis.

This is the context in which Hyperliquid's role should be evaluated. The protocol did not create demand for 24/7 oil trading — the demand existed the moment Iran's airspace was breached. It provided the only functioning venue where that demand could be expressed. JPMorgan's research team confirmed this was not a crypto-native phenomenon: the traders flooding into Hyperliquid's oil contracts that weekend were "particularly non-crypto" participants "seeking continuous exposure to assets like oil during periods when traditional markets are closed." They came because it was the only place open.

A Structural Shift, Not a One-Time Event

The tendency for geopolitical shocks to occur outside of traditional market hours is not an anomaly — it is a pattern. Wars escalate over weekends. Central bank interventions in the Middle East, Asia, and Eastern Europe are announced on Fridays after Western markets close. Currency crises unfold over holiday weekends. The 2026 Iran conflict merely made the cost of this pattern visible at a scale that could not be ignored.

Consider the implications for any allocator with commodity exposure. Before February 2026, the accepted risk management framework was that weekend gaps were tolerable because extreme events were rare. After February 2026, we have a documented case where the Strait of Hormuz — carrying 20-25% of global maritime oil — was effectively closed during a 49-hour market blackout, and the only functioning price discovery occurred on a decentralized exchange. The next geopolitical shock will occur on a weekend again. The question for allocators is whether they will have access to continuous hedging infrastructure when it does.

This is not an argument for or against any particular token. It is an observation about market structure. The 24/7 availability of on-chain commodity markets is a net-new capability that did not exist twelve months ago, and the Iran crisis demonstrated that the capability has real utility under precisely the conditions where traditional infrastructure fails. The Wall Street Journal, Bloomberg, and JPMorgan all reached the same conclusion independently — not because they are advocates of decentralized finance, but because the data from that weekend was unambiguous.

What 49,600 New On-Chain Traders Tell Us

Perhaps the most telling data point is not the volume figures but the composition of participants. In March 2026 alone, over 49,600 traders made their first-ever on-chain trade through Hyperliquid's HIP-3 markets — with nearly 20,000 entering through the Nasdaq 100 perpetual. These are not DeFi natives migrating from another protocol. They are traditional market participants who encountered a product that served a need their existing infrastructure could not.

The pattern is familiar to anyone who has studied technology adoption. Email did not replace the postal system because users wanted to use computers — it replaced it because the function was superior. Mobile banking did not succeed because users wanted to interact with an app — it succeeded because the bank branch was closed at the moment they needed it. On-chain commodity trading is following the same trajectory: the adoption is driven by functional necessity, not ideological preference.

For institutional allocators, this reframes the question. The relevant analysis is not whether decentralized exchanges will "disrupt" traditional markets — that framing is speculative and unhelpful. The relevant analysis is whether the demonstrated capability of 24/7 on-chain price discovery for commodities, equities, and indices represents a permanent expansion of available market infrastructure. The evidence from February and March 2026 suggests that it does.

Implications for Portfolio Construction

The existence of continuous commodity markets changes the hedging calculus for any portfolio with energy, metals, or equity index exposure. Weekend gap risk — historically accepted as an unhedgeable cost of holding commodity positions through a Friday close — is now a variable that can be managed in real time. This does not eliminate the risk; perpetual contracts carry their own basis risk, funding rate dynamics, and counterparty considerations. But it introduces an option that was previously unavailable.

The S&P 500 licensing deal with TradeXYZ extends this logic beyond commodities. If the world's most widely tracked equity benchmark is now available as a 24/7 on-chain perpetual, and if over 550 traditional financial institutions already hold S&P index licenses, the boundary between "crypto markets" and "traditional markets" is no longer a meaningful distinction for portfolio construction purposes. The relevant distinction is between markets that close during crises and markets that do not.

We present this analysis not as advocacy for a particular allocation, but as a framework for evaluating a structural development that we believe our LP base should understand. The February 2026 weekend was a proof-of-concept for continuous on-chain market infrastructure. Whether that proof-of-concept scales into a permanent feature of global markets — and how allocators should position for that outcome — is the question this memo is designed to inform.

Protocol Fundamentals

Hyperliquid's resilience under geopolitical stress is not accidental — it is the product of deliberate architectural decisions and a founding philosophy rooted in first-principles engineering.

Leadership and Founding

Hyperliquid was founded by Jeff Yan, a Harvard-educated mathematician and International Physics Olympiad gold medalist whose background at Hudson River Trading (HRT), one of the world's preeminent high-frequency trading firms, provided the quantitative depth required to build a low-latency exchange from first principles. The collapse of FTX in November 2022 was the catalyst: Yan and his team had consciously avoided FTX, and the bankruptcy crystallized his conviction that the market needed a transparently decentralized, high-performance trading venue.

"Centralized exchanges had a really great UX, and almost all the volume was happening on centralized exchanges, but no one in DeFi was really trying to match that."

— Jeff Yan, Fortune, January 2026

Critically, Hyperliquid Labs — a team of just 11-14 employees — turned down investment from Paradigm and Founders Fund. The protocol was bootstrapped entirely with profits from Chameleon Trading, Yan's prior HFT operation. This is not a token of frugality; it is a philosophical position. As Yan stated: VCs holding large stakes create an "illusion of progress" and act as a "scar on the network." The result is a protocol with $843 million in FY2025 revenue and zero VC dilution — a revenue-per-employee figure of approximately $76 million, which exceeds Goldman Sachs and Binance by an order of magnitude.

Technical Architecture

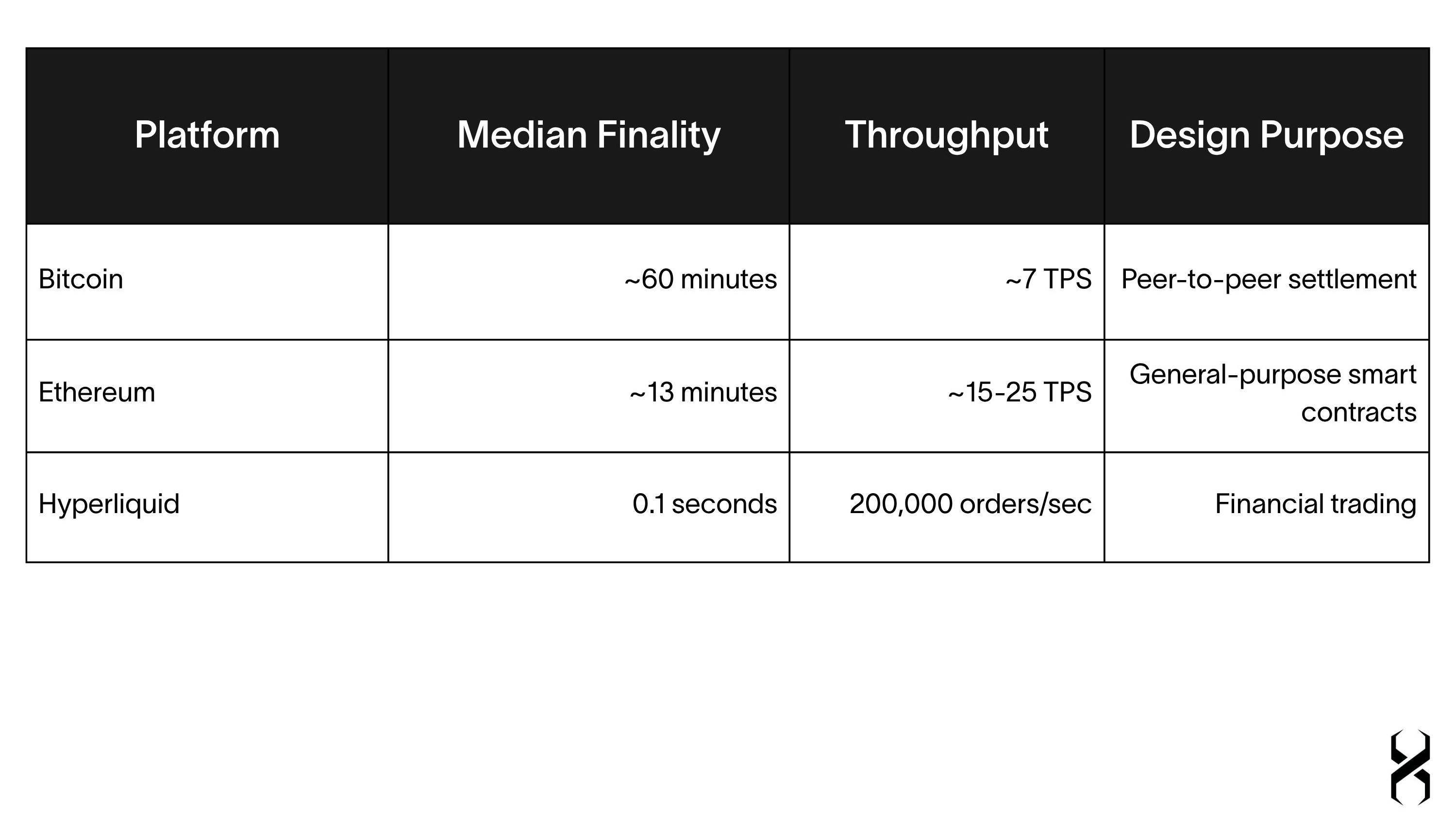

The protocol uses HyperBFT, a custom Byzantine Fault Tolerant consensus algorithm inspired by HotStuff, achieving one-block finality with sub-second latency. The HyperCore engine is a fully on-chain Central Limit Order Book (CLOB) — every order, cancellation, trade, and liquidation is executed natively on-chain with no off-chain matching layer. The Dual Block Structure (2-second fast blocks for trading, 60-second slow blocks for complex deployments) decouples latency from capacity. The HyperEVM layer provides Ethereum-compatible smart contract functionality with unified state — when HyperCore updates a price, the EVM sees it instantly in the same block, eliminating bridge risk and oracle lag.

The HIP Expansion Engine

HIP-1 (Token Standard): Native capped-supply token standard with a 31-hour Dutch auction listing mechanism.

HIP-2 (Hyperliquidity): Automated liquidity embedded in L1 logic, guaranteeing a 0.3% spread every 3 seconds for new listings — no external market makers required.

HIP-3 (Builder-Deployed Perpetuals): The most consequential expansion. Any entity staking 500,000 HYPE can deploy permissionless perpetual futures markets with custom oracles and fee structures — enabling oil, gold, silver, equity, and index perpetuals.

HIP-4 (Prediction Markets): Binary outcome contracts settled in USDH, live on testnet since March 10, 2026.

The Exchange of Everything

The strategic shift from crypto-native trading to the vertical integration of traditional assets was accelerated by HIP-3's launch in October 2025. Among the top 30 HIP-3 markets, only 7 are crypto pairs — the remaining 23 are traditional assets. Hyperliquid is no longer a crypto exchange that happens to list equities; it is becoming an everything exchange with crypto as just one product category.

TradeXYZ: The Primary Builder

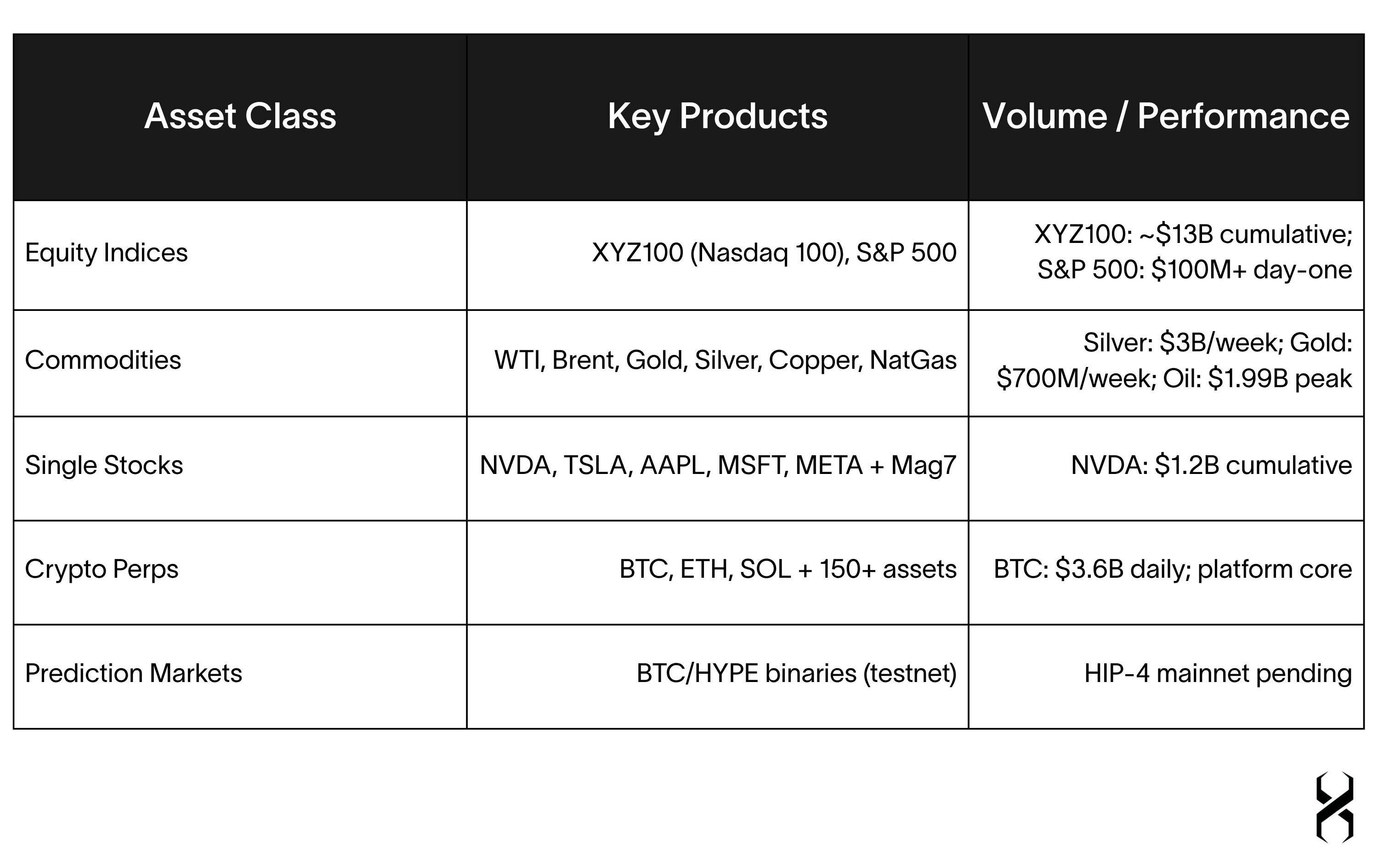

TradeXYZ (developed by Hyperunit) functions as a sub-exchange built on the Hyperliquid L1, accounting for approximately 90% of HIP-3 open interest with $105.6 billion in cumulative volume and an annualized fee run rate of $80 million.

The S&P 500 Milestone

On March 18, 2026, S&P Dow Jones Indices issued a formal press release announcing it had licensed the S&P 500 to TradeXYZ for the first and only officially licensed perpetual derivative contract based on the index. This is the first time in the 69-year history of the S&P 500 that the benchmark has been licensed for deployment on a decentralized platform. The contract hit $100 million in 24-hour volume within days of launch, and HYPE surged 14.7% on the news. Over 550 financial institutions worldwide hold S&P index licenses — TradeXYZ is the first on-chain entity to join that list.

Product Landscape

From a single USDC margin account, a trader can now access crypto perpetuals, commodity futures, equity exposure, index products, and soon prediction markets — 24 hours a day, 365 days a year, with no broker, no KYC, and no settlement delay. The HIP-3 framework means the product catalog is permissionlessly expandable: any builder can deploy new markets without Hyperliquid's direct involvement, provided they stake the required 500,000 HYPE. This is the structural moat — the platform's product depth grows without the team needing to build it.

Competitive Positioning

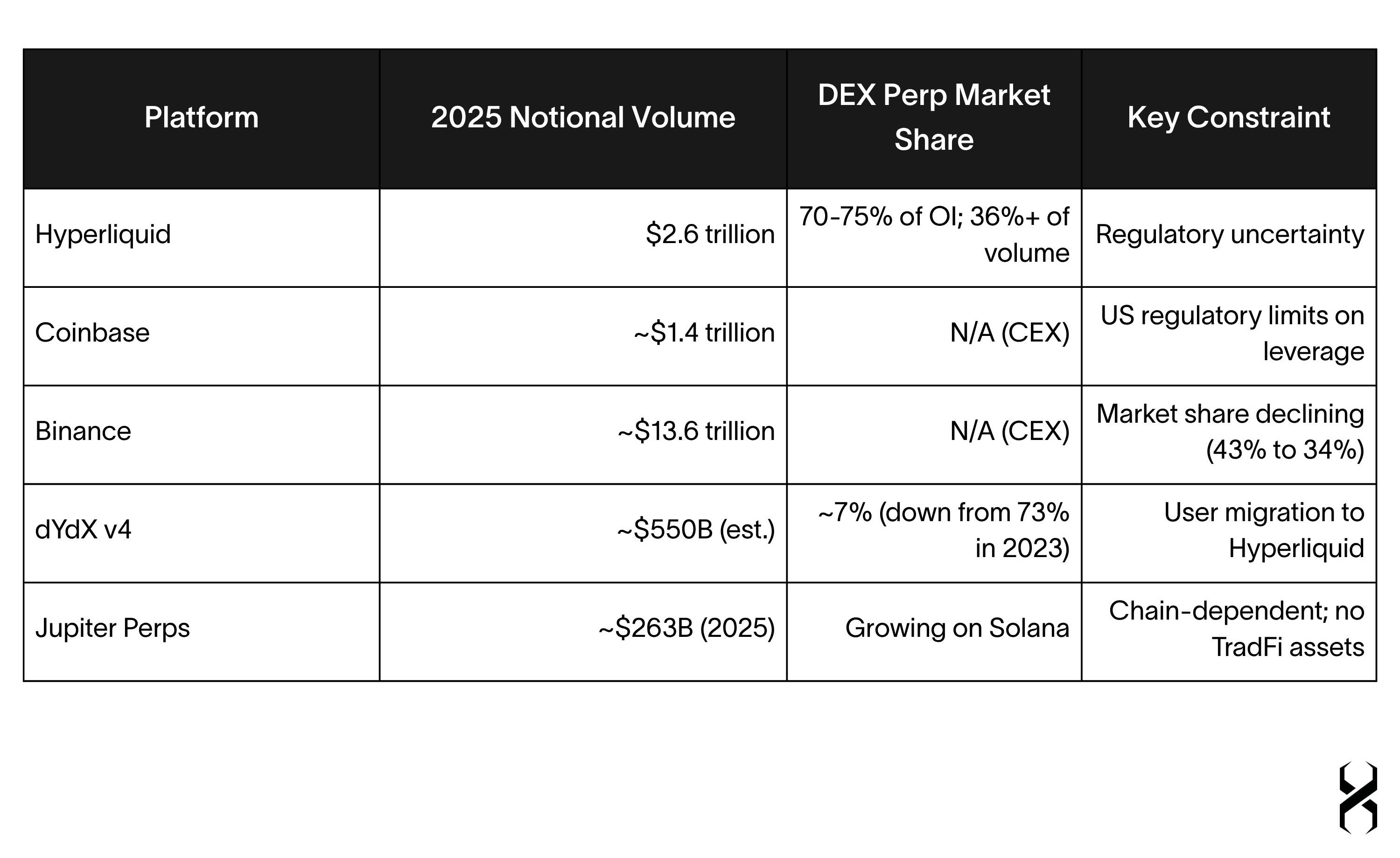

The DEX-to-CEX Shift

The decentralized derivatives market has undergone a structural transformation. DEX perpetual futures volume grew 8x from $81.7 billion to $739.5 billion monthly, with market share expanding 5x from 2.0% to 10.2%. Critically, while CEX open interest fell 20.8% in 2025, DEX open interest surged 229.6% — a divergence that signals long-term capital commitment to decentralized infrastructure, not episodic speculation. Hyperliquid crossed $4 trillion in cumulative all-time volume by March 2026, with acceleration telling the story: the first $1 trillion took 733 days; the third took just 88 days.

Hyperliquid vs. The Field

Hyperliquid's 2025 volume was nearly 2x that of Coinbase — a remarkable benchmark given Coinbase is a publicly listed, regulated U.S. entity with over $3 billion in annual revenue. The asymmetry exists because Coinbase's regulatory framework restricts high-leverage derivatives products, while Hyperliquid's decentralized model offers up to 50x leverage on certain assets with 24/7 access to non-crypto markets that no CEX currently provides.

The structural advantages are compounding: a purpose-built L1 eliminates bridge risk, a fully on-chain CLOB provides CEX-grade execution, HIP-3's permissionless market creation means product depth grows without central coordination, and the absence of VC funding means no unlock overhang diluting existing holders. These are not features that competitors can replicate by adding a feature — they are architectural decisions made at the protocol's inception.

HYPE Token: The Investment Case

We frame HYPE not as a governance token but as a productive asset tied to the most efficient fee-capture machine in decentralized finance.

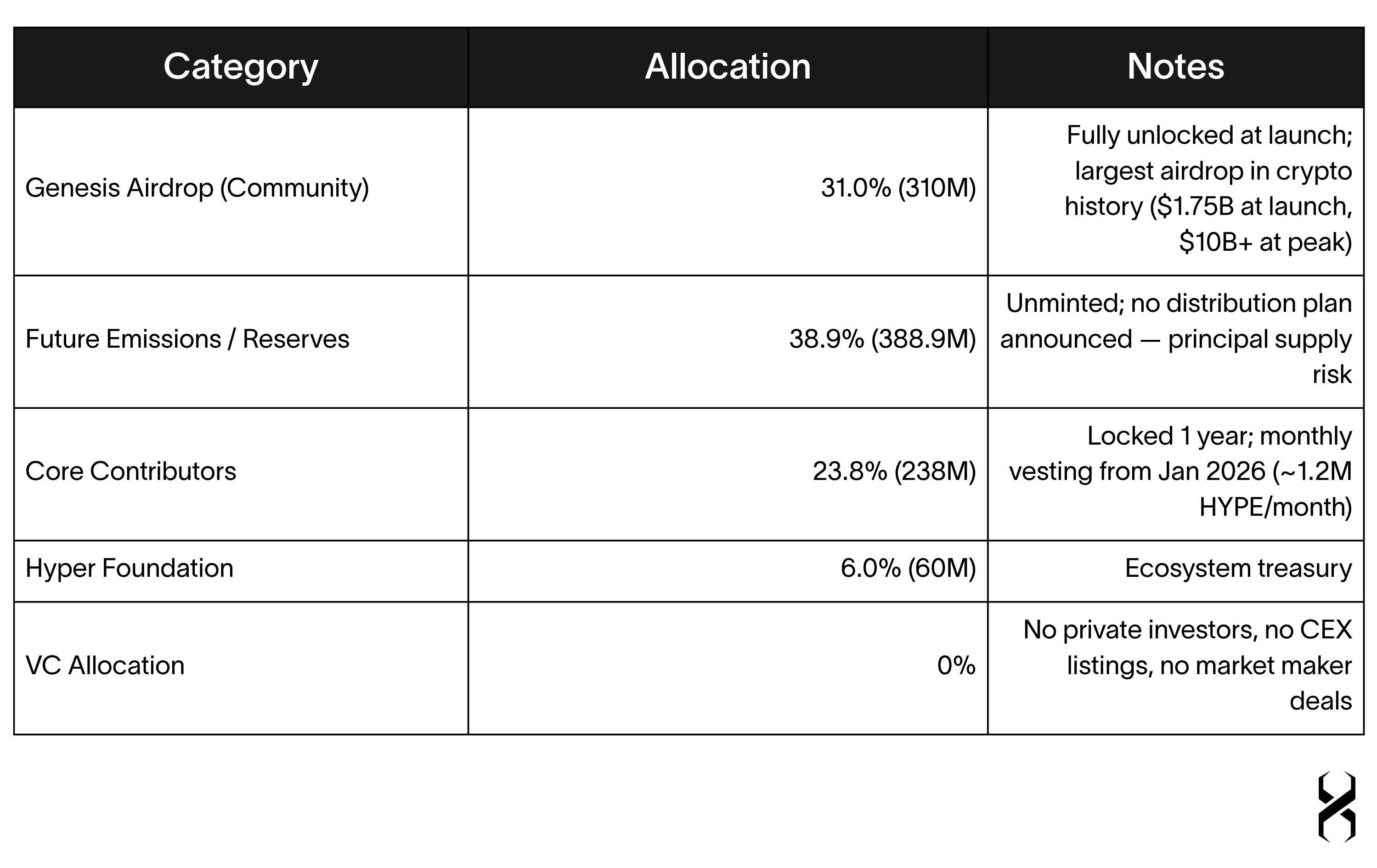

Tokenomics

Revenue and Buyback Flywheel

Hyperliquid generated $843 million in revenue in FY2025, making it the second-largest revenue-generating blockchain globally — behind only Solana (~$1.3-1.4B) and ahead of Ethereum (~$524M). The Assistance Fund automatically converts approximately 97% of trading fees into HYPE buybacks and permanent burns, sending tokens to a controlled address with no private key. As of March 2026, approximately $1.35 billion worth of HYPE (41.7 million tokens) has been permanently destroyed. This creates a direct, mechanical link between trading volume and token scarcity — one that requires no management decisions, no board votes, and no timing discretion.

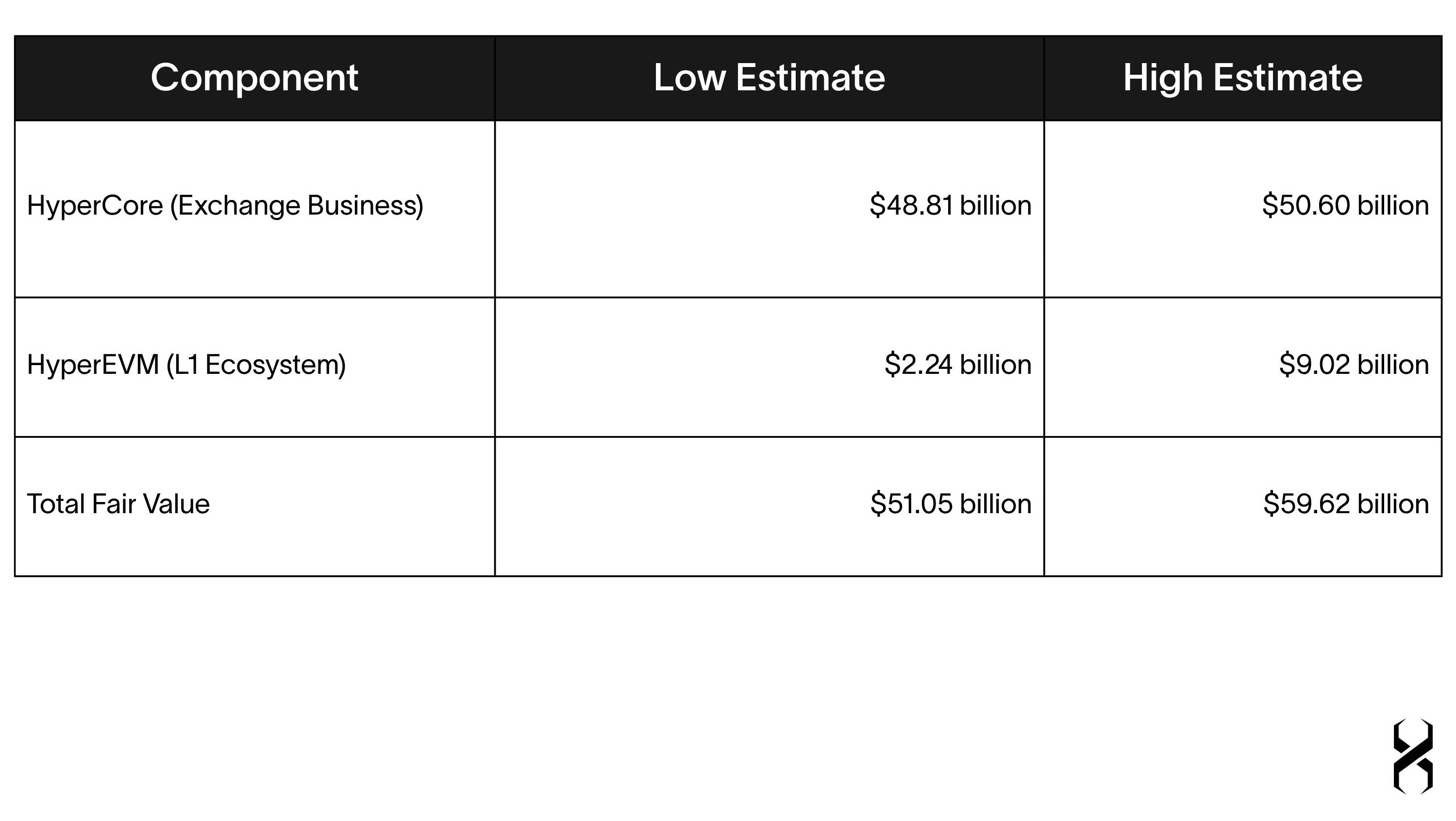

Valuation

The Artemis sum-of-the-parts model values the core exchange business at $48.8-50.6 billion based on earnings multiples derived from Coinbase and Robinhood, with the HyperEVM layer valued separately at $2.2-9.0 billion using fee-to-valuation ratios from Solana and Ethereum. At current market capitalization, HYPE trades at an estimated 35-40% discount to listed exchange peers — a gap that reflects regulatory uncertainty and the market's underappreciation of the non-crypto revenue stream now emerging through HIP-3.

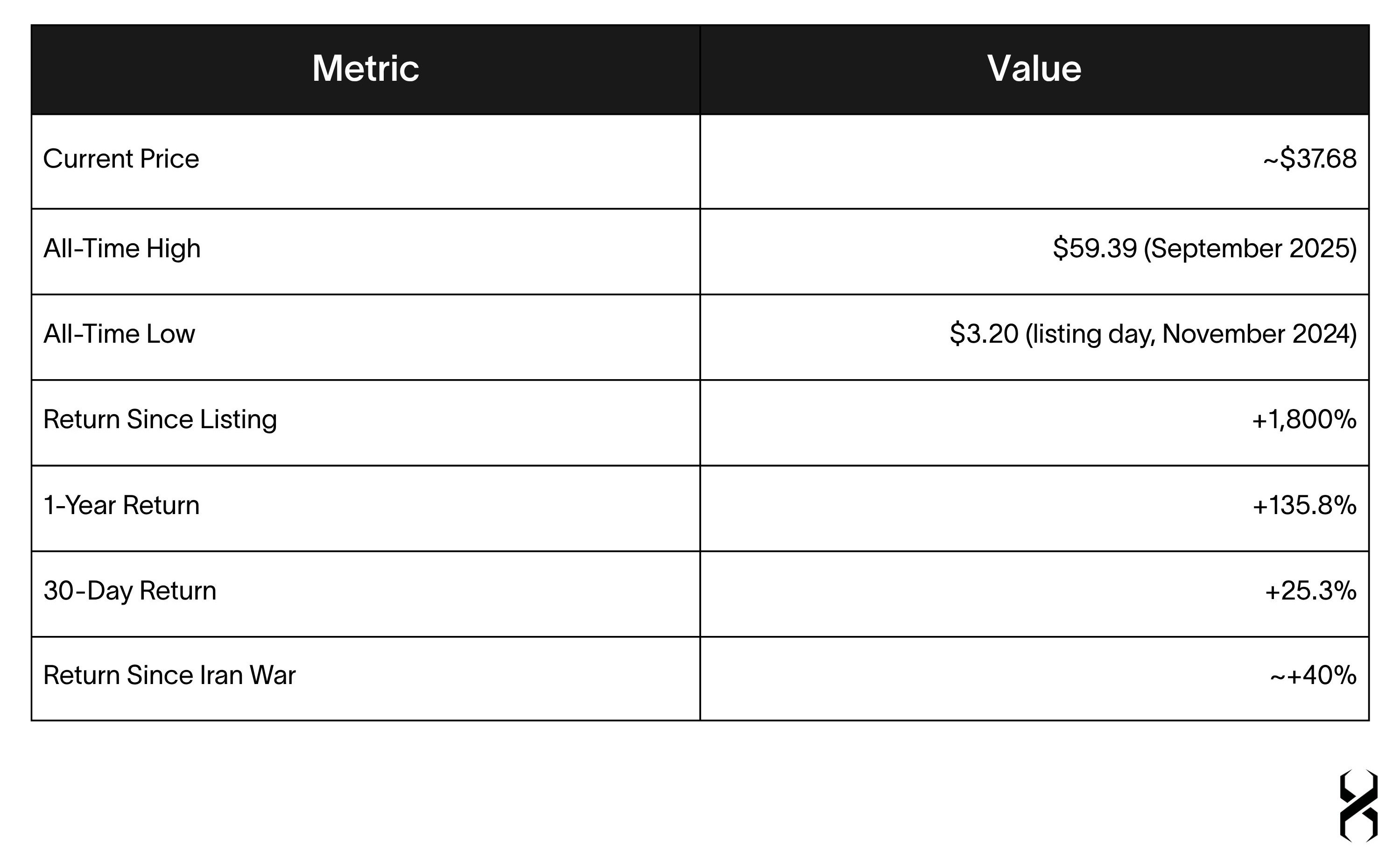

Price Performance

The Bear Case: Intellectual Honesty

Supply Overhang: 38.9% of total supply remains unminted with no announced distribution plan, representing approximately $15 billion in potential future dilution at current prices.

Volume Cyclicality: A material portion of recent volume is tied to the Iran conflict. A de-escalation could see commodity perp volumes retreat from $1.99B/day toward the $21M baseline — a 95% decline that would proportionally reduce fee revenue.

Security Incidents: The JELLY attack (March 2025, $12M at risk), the POPCAT exploit ($4.9M HLP loss), and the ETH margin exploit ($4M loss) represent a recurring pattern of manipulation targeting the backstop liquidity pool.

Risks and Considerations

Regulatory Exposure: Perpetual futures sit in an unresolved regulatory category globally. The CFTC Chair stated in March 2026 that a framework for crypto-linked perpetual futures is coming "within weeks." The platform's absence of KYC — while a product feature for users — is its most acute regulatory liability.

Geopolitical De-escalation: A diplomatic resolution to the Iran conflict would compress implied oil volatility and reduce the demand for leveraged commodity exposure. Hyperliquid has not published a volume decomposition between structural and cyclical demand.

Validator Centralization: Hyperliquid operates with 16 validators, with the Hyper Foundation controlling approximately 80% of staked HYPE. The L1 node software remains closed-source.

Discovery Bounds: Hyperliquid uses Discovery Bounds to limit price deviation from reference prices during after-hours trading (±15.8% total range, ±5% instantaneous caps). While necessary for risk management, these bounds become the primary constraint on price discovery during extreme weekend moves — potentially limiting the platform's effectiveness as a true primary discovery venue for moves exceeding 15%.

Competition Adapting: The New York Stock Exchange and ICE have announced plans for 24/7 trading platforms. However, the structural advantages of a purpose-built L1 with fully on-chain execution and permissionless market creation cannot be replicated by adding a feature to an existing platform.

Axys View: What This Means for Our Readers

We write this memo not to advocate for a position but to document a structural shift in market infrastructure that we believe our LP base and stakeholders should evaluate independently.

The central observation is straightforward: when every traditional commodity exchange in the world was dark for 49 hours during the most significant geopolitical crisis since the Russian invasion of Ukraine, a decentralized protocol built by 11 people processed 91,000 oil trades and priced 78% of the CME's Monday opening move before legacy markets quoted a single tick. The Wall Street Journal put it on the front page. JPMorgan published a research note. Goldman Sachs revised forecasts while Hyperliquid was already pricing the new reality in real time.

The question this raises is not whether crypto is "good" or "bad" — that framing is irrelevant. The question is whether global market infrastructure has permanently expanded to include 24/7 on-chain venues for commodities, equities, and indices. The evidence suggests that it has. Over 49,600 new traders entered on-chain markets in March 2026 alone — not because they wanted to use a blockchain, but because they needed to hedge oil exposure on a Sunday night and there was nowhere else to do it.

For portfolio construction, this introduces a variable that did not exist twelve months ago. Weekend gap risk in commodities — historically accepted as unhedgeable — is now manageable through perpetual contracts that trade continuously. The S&P 500 is available as a licensed 24/7 derivative for the first time in the index's 69-year history. The boundary between crypto markets and traditional markets is dissolving, and the pace of that dissolution accelerated dramatically in February 2026.

Hyperliquid sits at the center of this development for reasons we have documented: purpose-built architecture, $843 million in annual revenue, permissionless market creation through HIP-3, and the demonstrated ability to function as primary price discovery infrastructure during a genuine crisis. The HYPE token is a direct claim on this revenue through a 97% buyback mechanism, trading at what Artemis estimates is a 35-40% discount to listed exchange peers.

As Fund Managers our role is to identify structural shifts early, evaluate them rigorously, and present our findings to the people who trust us with their capital. The February 2026 weekend changed the landscape for on-chain market infrastructure.

Disclaimer

This material is provided for information purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any financial product or service in any jurisdiction.

The views expressed are those of the author as at the date of publication and are subject to change without notice. While reasonable care has been taken, no representation or warranty, express or implied, is made as to the accuracy, completeness, or reliability of the information contained herein, and no reliance should be placed upon it.

This material has not been reviewed or approved by the Dubai Financial Services Authority, the British Virgin Islands Financial Services Commission, or the Cayman Islands Monetary Authority, or any other regulatory authority.

This material is not intended for distribution to, or use by, any person in any jurisdiction where such distribution or use would be contrary to local law or regulation. In particular, this material does not constitute a public offer of securities in the British Virgin Islands or the Cayman Islands.

Any investment or service referred to herein will be available only to persons who meet the relevant eligibility criteria under applicable laws and regulations, including, where applicable, Professional Clients (as defined by the Dubai Financial Services Authority) or other equivalent categories of sophisticated or professional investors under applicable law.

Investments involve risk, including the possible loss of capital. Past performance is not a reliable indicator of future results.

“Axys” is a trading name used by a network of independent businesses. Axys does not operate as, and is not, a separate legal entity in any jurisdiction and has no distinct legal personality. Each business operating under the Axys name is independently owned and operated.

Axys Capital Ltd is authorised and regulated by the Dubai Financial Services Authority. Axys Investment Management Ltd is authorised and regulated by the British Virgin Islands Financial Services Commission.